The TAM for Intelligence is Infinity

Every major technology wave of the last 50 years gave humans a better tool. Intelligence is different in kind, not just degree — because for the first time, the tool begins to direct itself.

Intelligence is the largest market that will ever exist. There is no analogy that quite captures it. But here's the closest one:

Take the sum total of every thought that every person on earth will ever have from this moment forward, add every word ever written by a human or a machine, and you start to approach the scale of what is actually at stake.

That is the feedstock of intelligence. And intelligence — packaged, sold, and delivered at scale — is the product being built right now.

This is not a sector. It's not a theme. It is the single largest market opportunity that has ever existed or ever will.

The dominant vendors — OpenAI, Anthropic, Google, Microsoft, Amazon — understand this perfectly. Which is why the thing that should actually unnerve them isn't each other. It's OpenClaw.

OpenClaw is an open-source agentic AI platform that hit 9,000 GitHub stars in its first 24 hours after launching in November 2025 and crossed 214,000 by February 2026 — faster than Docker, Kubernetes, or React ever grew. Between 300,000 and 400,000 people are actively running it now.

As an early operator, I've rebuilt my stack on it five times and about to again.

It is genuinely that important.

Here's why the big players are doing more than just paying attention

Open-source doesn't just commoditize the product layer — it systematically dismantles the revenue model.

- Linux didn't kill Microsoft overnight, but it permanently capped what Microsoft could charge for server software and forced a 20-year pivot to services.

- Android didn't kill Apple, but it made the smartphone operating system functionally free for everyone else and handed Google a distribution moat that no carrier or handset maker could replicate.

When the orchestration layer is open-source, when memory is owned by the operator rather than the platform, when skills can be community-built and freely distributed, the VC-subsidized token economics that currently make the big platforms cheap enough to be sticky start looking like a temporary competitive position rather than a permanent moat.

OpenClaw is about owning intelligence instead of renting a vendor's primary moat

OpenClaw is positioning to do something similar to Android or Linux at the intelligence layer — except the market it's threatening is orders of magnitude larger than either of those. Anthropic's latest event, Code with Claude, was full of features and initiatives that attempt to capture the lock-in of intelligence within their ecosystem.

IBM Research scientists who analyzed OpenClaw concluded it directly challenges the assumption that autonomous AI agents must be vertically integrated. That architectural choice — owning the stack versus renting it — is where the long-term battle for the intelligence market will be decided.

More on that in a moment.

The Infrastructure Running Out of Room

Start with the physical constraint, because it tells you everything about demand.

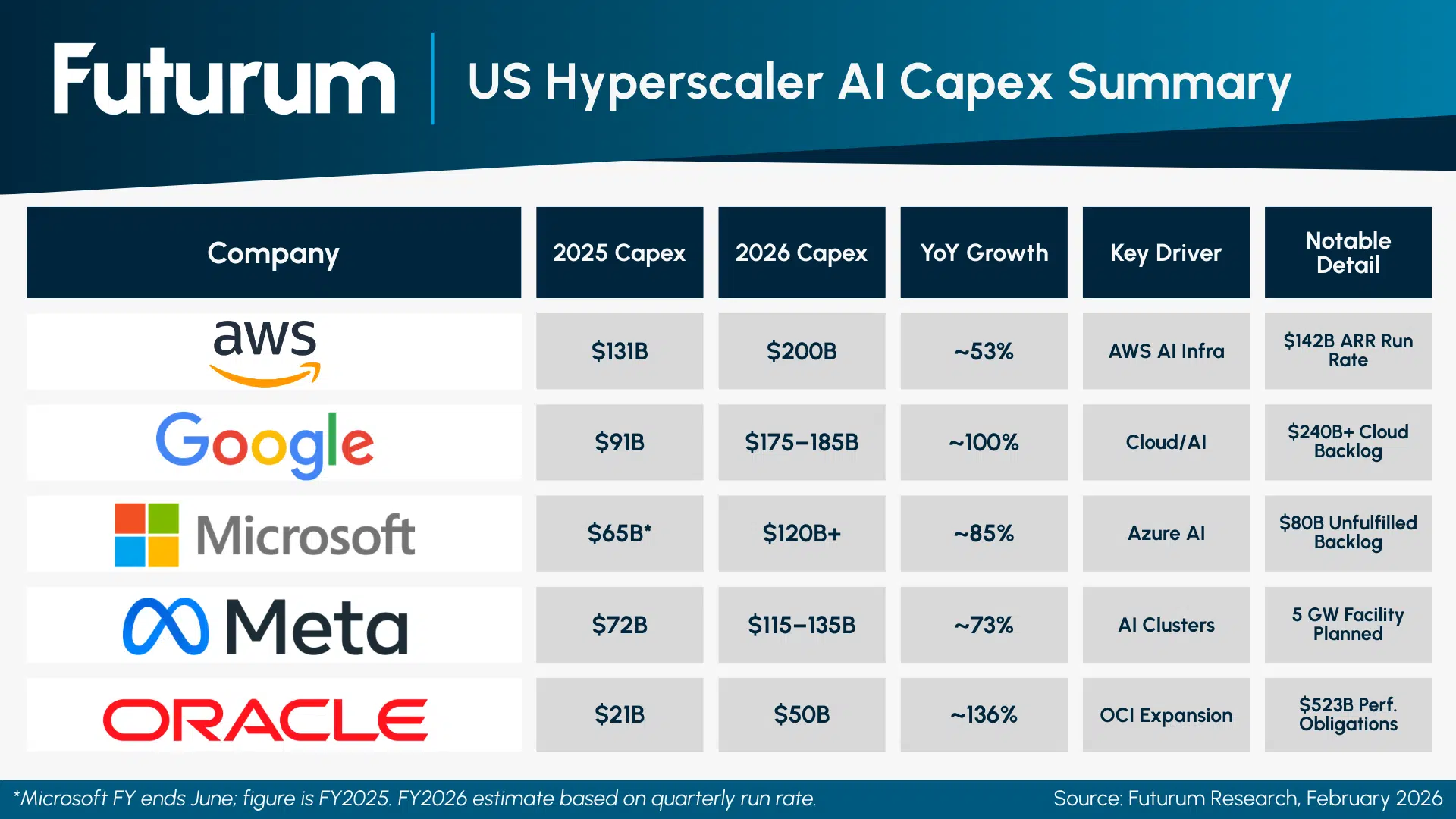

The five largest US cloud and AI infrastructure providers — Microsoft, Alphabet, Amazon, Meta, and Oracle — have collectively committed to spending between $660 and $690 billion on capital expenditure in 2026, nearly doubling 2025 levels.

Amazon alone has projected $200 billion in 2026 capex, the majority directed at AI infrastructure. AWS added 3.9 gigawatts of new power capacity in 2025 and expects to double its total power capacity by the end of 2027. The International Energy Agency now projects that global data center electricity consumption will exceed 1,000 terawatt-hours by the end of 2026 — the equivalent of Japan's entire annual electricity usage.

None of this is speculative. Every hyperscaler is reporting the same problem: capacity installed is consumed before it's even fully operational.

Andy Jassy said it plainly during Amazon's Q1 2025 earnings call: as fast as new capacity comes online, it gets absorbed. AWS's AI revenue run rate crossed $15 billion in Q1 2026 — a figure Jassy noted is nearly 260 times larger than what AWS itself had reached at the same point in its lifecycle as a cloud business. That number was considered astronomical at the time. It now looks like an early data point.

The revenue trajectory on the model side is even harder to rationalize in conventional terms. Anthropic went from a $9 billion annualized revenue run rate at the end of 2025 to over $30 billion by April 2026 — more than tripling in roughly four months, overtaking OpenAI's approximately $25 billion ARR in the process. More than 1,000 enterprise customers now spend over $1 million per year with Anthropic, a count that more than doubled in less than two months following the company's Series G raise. OpenAI, meanwhile, is approaching 900 million weekly active users and ChatGPT is on track to cross 1 billion — a milestone that, if reached, would make it one of the most rapidly adopted technologies in the history of consumer software.

The bears' argument — that the infrastructure spend is reckless, that returns aren't materializing, that this looks like the dot-com build-out — runs directly into these numbers.

Revenue is materializing. Demand is outrunning supply. The constraint is electrons, not customers.

The Largest TAM Ever Built

Here is the framing that actually holds up analytically.

Every major technology wave of the last 50 years — the personal computer, the internet, the web, mobile, cloud, SaaS — created enormous markets by expanding access to a specific capability. The PC gave individuals computing power. The internet gave individuals connectivity. Mobile gave individuals always-on access. Each wave was transformative. Each created trillion-dollar industries.

Intelligence is different in kind, not just degree.

Same same, but different

Every one of those prior waves was a tool that required a human to direct it. Intelligence, as it's being built now, begins to direct itself. It doesn't just accelerate human effort — it begins to substitute for it, augment it, and in some cases, make categories of human decision-making optional.

The practical implication is that every business on earth becomes a customer. Not as an experiment. Not as a pilot program. As a structural requirement for competitive survival.

Intelligence will become a first-class entity and not as a subset of technology — as its own distinct operating layer. The companies that treat AI as a tool being layered onto existing workflows will find themselves structurally disadvantaged against the ones that build intelligence into how the business actually runs.

That shift makes the total addressable market for intelligence effectively unbounded.

You're not selling software to companies that need software. You're selling a new input — one that every productive enterprise in every sector on earth will eventually require, in the same way they require people and capital.

There is no historical category for that TAM.

The Adoption Problem Is the Real Problem

Here is where optimism needs to meet operational reality.

The supply-side story is staggering and getting more so. The demand-side story is equally clear. The gap between those two and the actual transformation of existing enterprises is where the decade of work lives.

I've outlined a four-project AI adoption system because adoption will likely remain the largest single obstacle to the intelligence transition. Not access. Not cost. Not model capability.

Without adoption, you have no integration. Without integration, you have no transformation. The risk is that AI stays siloed — a department tool, a productivity experiment, a check-box for the board deck. Companies will be able to say they use AI without being meaningfully changed by it. That gap will be ruthlessly exposed.

This is not a fast process. The integration of intelligence as a genuine operational pillar — embedded in how decisions are made, how products are built, how customers are served — is a multi-decade evolution for most established businesses.

It will not happen through a single implementation project or a technology refresh cycle. It requires rebuilding how the organization thinks about its own operating model.

That is slow work. The technology is moving faster than any organization can absorb it. That mismatch is where the risk concentrates.

The Shareholder Metric That Doesn't Exist Yet

Markets are already pricing the early signals of AI disruption, sometimes crudely.

When Anthropic rolled out new enterprise automation capabilities earlier this year, software stocks moved violently in response. Adobe, Salesforce, and ServiceNow each declined 25% to 30% in the first months of 2026. The iShares Expanded Tech-Software Sector ETF dropped more than 14% over six sessions following one announcement. Software sentiment, according to a Jefferies note at the time, was described as the worst ever.

This is the market beginning to price AI exposure — but doing it bluntly, using fear of disruption as the primary signal rather than any concrete measure of transformation progress.

The disclosure infrastructure hasn't caught up.

Public companies are now labeling AI in shareholder documents. That's the first stage. We are not yet at the next stage where filings routinely report a few new concepts:

- What percentage of core processes have been automated by agents, and

- what share of net new revenue is attributable to offerings that didn't exist without AI, or

- what the trajectory of per-unit intelligence costs looks like over time.

Those metrics don't exist yet in standard disclosure frameworks.

They will. And when they do, the rate of AI adoption and integration will become among the most consequential shareholder metrics in use. Not because analysts decide it's important, but because the companies that move fastest on this dimension will structurally outperform the ones that don't — and that will eventually show up in every line of the income statement.

The byproduct of that dynamic

We may see the shortest S&P 500 ascents and fastest index exits of any era on record. Companies that have genuinely integrated intelligence into their operating model will scale faster than anything in the prior four decades. Companies that didn't take it seriously — that kept it siloed, that counted AI mentions in their 10-K as strategy — will compress.

The laggards won't announce their own obsolescence. That's only ever knowable in hindsight.

The Only Question That Actually Matters

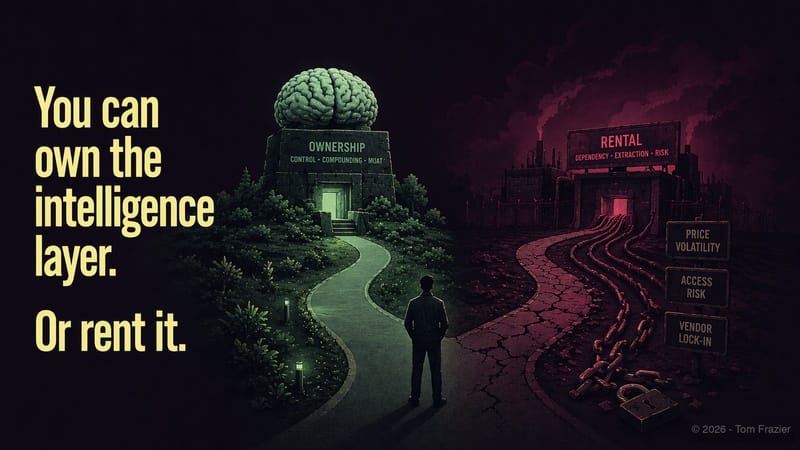

I said earlier that the long-term battle for the intelligence market will be decided by the ownership question. Here it is, stated as plainly as I can:

Who owns your intelligence?

Not your AI tool. Not your subscription. Not your workflow automation. Your intelligence — the accumulated decisions, context, institutional knowledge, and memory your organization generates every day when it operates and when it reasons.

If that intelligence lives on someone else's platform, you're not building a fourth pillar. You're renting one.

And when the terms change — the pricing, the data policies, the model updates, the platform access — you'll have no leverage, because the moat belongs to the vendor, not to you.

I've written about the fourth pillar of business at length: intelligence is no longer a feature of technology, it's a distinct operating layer that sits alongside people, process, and technology. Companies that treat it that way will build something compounding and proprietary. Companies that don't will remain dependent on whoever controls the platform.

This is the promise of open-source orchestration layers

The platform incumbents should be uncomfortable with its growth trajectory. If a business can own its memory, direct its own agents, and swap the underlying model based on task and cost rather than platform lock-in,

the VC-subsidized access economics that currently make ChatGPT and Claude cheap enough to be sticky become a much weaker argument for staying.

Linux and Android taught us that open-source doesn't have to win on every dimension to permanently reshape the economics of a market. It just has to win on the dimension that matters most to the builder. For the intelligence market, that dimension is ownership.

Every business leader making AI decisions right now should answer one question before anything else:

if your AI platform disappeared tomorrow, what would you still have?

If the answer is "not much," then the transformation hasn't happened yet — you've just moved a cost center. The companies that will define the next decade of enterprise performance are the ones building intelligence they actually own, as an asset that compounds in their favor rather than in the vendor's.

The TAM for intelligence is effectively infinite. The question of who captures it — the platforms, the open-source operators, or the enterprises that figure out how to own their own stack — is the most consequential strategic question in business right now.

If your answer to "who owns your intelligence?" is anything other than we do, you have a problem that no amount of AI spend will fix.