GTC 2026 Proves Vera Rubin Changes the Conversion Math... Mid-Tier Miners Are Now Obvious Acquisition Targets.

An acquirer buying distressed mining equity at a 20 to 30% premium to market cap is almost certainly paying less per megawatt than a greenfield build — and they're getting an asset that can be operational in months rather than years.

In 2023, I was operating the Redivider Opportunity Zone Fund — a vehicle built around a specific thesis: 1 - Edge computing for Bitcoin mining and AI compute were converging, and 2 - Opportunity Zones offered an unusually clean structure for building that convergence with tax-advantaged capital. The core bet was that purpose-built, energy-dense facilities in underserved markets would become critical infrastructure before most investors recognized them as such. We got the first part right but the Opportunity Zone model was too restrictive to raise enough capital to be effective.

However the massive requirement for power is now beyond consensus. IREN signed a $9.7 billion deal with Microsoft. Hut 8 locked up a 15-year, $7 billion hosting agreement tied to Anthropic. CleanSpark crossed 1.4 gigawatts of contracted power. The hyperscalers got there first, and the miners who moved early are now partly valued as infrastructure companies rather than Bitcoin price proxies.

This is part two of that thesis. The first trade has been made. The second trade is sitting in plain sight, and it's still mispriced.

What's Left on the Table

The tier-one miners are fine. They've signed their deals, repriced accordingly, and have sophisticated management teams actively managing the transition. Trying to acquire them is expensive and contested.

But beneath that tier sits a cohort that most analysts aren't focused on: publicly traded mid-tier miners with 100 to 500 megawatts of contracted, permitted, substation-connected power — and no anchor HPC tenant. These operators haven't signed a hosting deal. They're running on compressed margins in a market where hashprice fell roughly 35% from mid-2025 to late 2025. Their stock prices reflect Bitcoin's recent slump, not the underlying value of their power infrastructure.

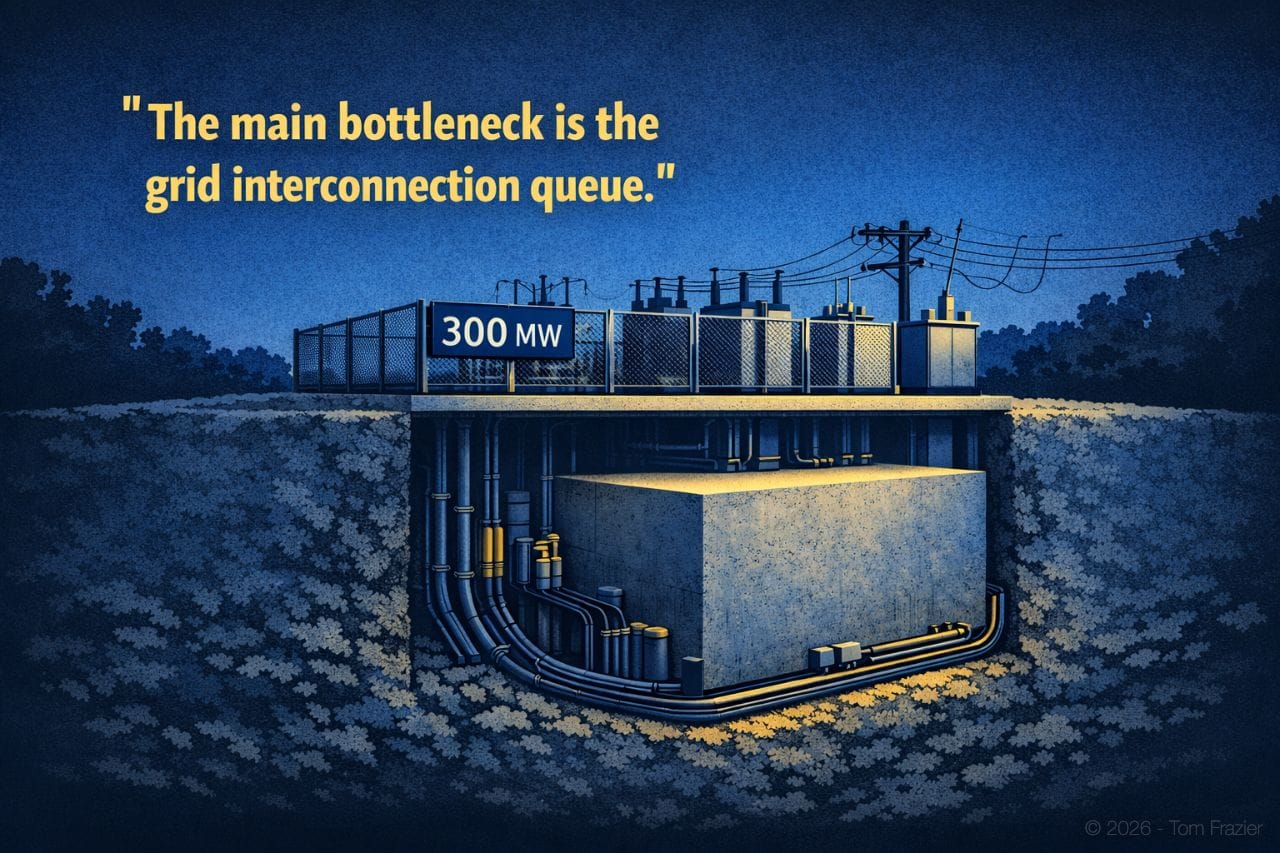

The bottleneck for new AI data centers is no longer capital or construction. The main bottleneck is the grid interconnection queue, which runs five to ten years in the most congested markets.

A mid-tier mining site bypasses that queue entirely. The interconnection rights exist. The substation is built. The site is permitted and zoned for exactly the kind of high-density power consumption that AI clusters require.

AI data centers generate up to 25 times more revenue per kilowatt-hour than Bitcoin mining.

An acquirer buying distressed mining equity at a 20 to 30% premium to market cap is almost certainly paying less per megawatt than a greenfield build — and they're getting an asset that can be operational in months rather than years.

That's the trade. The question has always been execution, and that question just got materially easier to answer.

The Cooling Objection Is Gone

For years, the technical knock on mining-to-AI conversion was infrastructure incompatibility. Mining operations are built for ASICs: dense airflow, simple thermal management, no precision cooling requirements. Legacy (crazy to think that legacy here is measured in months not decades) AI training clusters — the conventional wisdom went — need chilled water loops, raised floors, tight environmental controls. Converting a mining facility wasn't just a hardware swap; it was a facility rebuild.

That argument is now substantially weaker, and the reason is NVIDIA.

Earlier this year, Jensen Huang made the architecture direction explicit: NVIDIA's next-generation Vera Rubin platform is designed to be cooled entirely via liquid cooling using warm facility water at temperatures up to 45°C. At that temperature, compressor-based chillers are unnecessary in most climates. Dry coolers and closed-loop ambient systems handle the load. The mechanical plant you'd need to build is dramatically simpler — and dramatically cheaper — than what traditional data center cooling has required.

This week at NVIDIA GTC 2026, that vision got a production product around it. Accelsius announced the NeuCool IR150: the industry's first fully integrated rack-level two-phase cooling solution. A single 800mm-wide enclosure ships with a CDU, 42U of rack space, and built-in liquid and vapor manifolds factory-tested and ready to deploy. It delivers 150kW of cooling capacity, uses a non-conductive dielectric refrigerant with zero water inside the rack, and is ASHRAE W45 compatible — meaning it's designed from the ground up for the 45°C warm-water world that Vera Rubin requires. Independent analysis has shown two-phase systems of this kind deliver 35 to 44 percent annual OpEx savings over single-phase alternatives.

I've got a lot of experience with immersion cooling and dielectric fluids. So, while personally I believe there is higher probability of failure or complication due to two-phase systems instead of single-phase, either dielectric option lends itself for the acquisition thesis. The liquid cooling matters precisely because it eliminates the facility rebuild argument.

The conversion path is now: existing power contract → dry cooler → integrated rack → GPUs. That's a weeks-long project. IREN's co-CEO said it directly — converting ASIC halls to GPU racks comes down to removing ASICs, removing the racks, and replacing them with standard data center racks. The hard part was never the hardware. It was the cooling. That problem now ships in a box.

Vera Rubin itself is expected in the second half of 2026, with 5x inference and 3.5x training performance improvements over Blackwell!

The AI companies that need to run those systems at scale need power. The infrastructure required to cool those systems is simpler than it has ever been. And there are Bitcoin miners sitting on exactly the right power assets, at exactly the wrong valuations, with no clear path forward.

What This Does to Bitcoin

Here's the part of this story that the Bitcoin community should think through carefully — and that most AI infrastructure coverage ignores entirely.

Bitcoin's hashrate hit a record 1 zetahash per second in 2025. The network has never been more computationally secure. Foundry USA commands roughly 25 to 30% of global hashrate, making it the dominant pool — but it's a US-based, regulated operation, and a pool is not a single entity. A 51% attack requires sustained, coordinated control that no realistic scenario puts within reach.

Now suppose 15 to 20% of current hashrate migrates off the network over the next two years as mid-tier miners sell their power infrastructure to AI operators. Bitcoin's difficulty adjustment responds automatically. Block times temporarily extend. Within two weeks, difficulty adjusts downward, and the remaining miners earn more per block. The operators who stay get a profitability tailwind precisely because the marginal operators left.

This dynamic is not theoretical. It played out after China's mining ban in 2021 — a sudden, massive hashrate reduction that temporarily disrupted block times, triggered the largest single difficulty adjustment in Bitcoin's history, and ultimately produced a more geographically distributed, more profitable mining industry. The network didn't break. It rebalanced.

The difference this time is that the reduction would be gradual and voluntary, concentrated among the least profitable operators at current prices. Bitcoin's difficulty adjustment was designed for exactly this. The miners who exit the network in exchange for AI infrastructure contracts aren't threatening Bitcoin's security — they're subsidizing the profitability of every miner who remains.

The Window

The combination of factors creating this opportunity is genuinely unusual:

- compressed Bitcoin prices reducing mining valuations,

- a cooling architecture that eliminates the primary conversion objection,

- a grid interconnection crisis that makes existing power rights more valuable than they've ever been, and

- a mid-tier cohort that hasn't yet signed away its optionality.

I thought this convergence was inevitable in 2023. The only thing I didn't know was the exact sequence of events that would make it obvious to everyone else. That sequence is now running.

The hyperscalers are not oblivious to what's left. Every month that passes is a month where a distressed miner either signs a hosting deal, finds its own HPC pivot, or gets acquired by someone who arrived at this conclusion earlier. The window for an aggressive acquirer to move on the distressed mid-tier — at mining valuations rather than infrastructure valuations — is measured in months, not years.

That was true in 2023 as a thesis. It's true today as an observation. The difference is that now there's no ambiguity about what these assets are worth, or who wants them.